ASIC Drills Down on Directors – Continuous Disclosure and Financial Record-keeping

09 Oct 2023

ASIC has warned market participants that strong, targeted enforcement action will continue in the coming months as part of its focus on protecting consumers and investors from harm and upholding market integrity.

The warning comes after ASIC’s recent enforcement and regulatory update highlighted over $109 million in civil penalties for the half year to 30 June 2023.[1]

In this context, ASIC continues to clamp down on corporate misconduct by targeting the directors and officers that are responsible for corporate breaches.

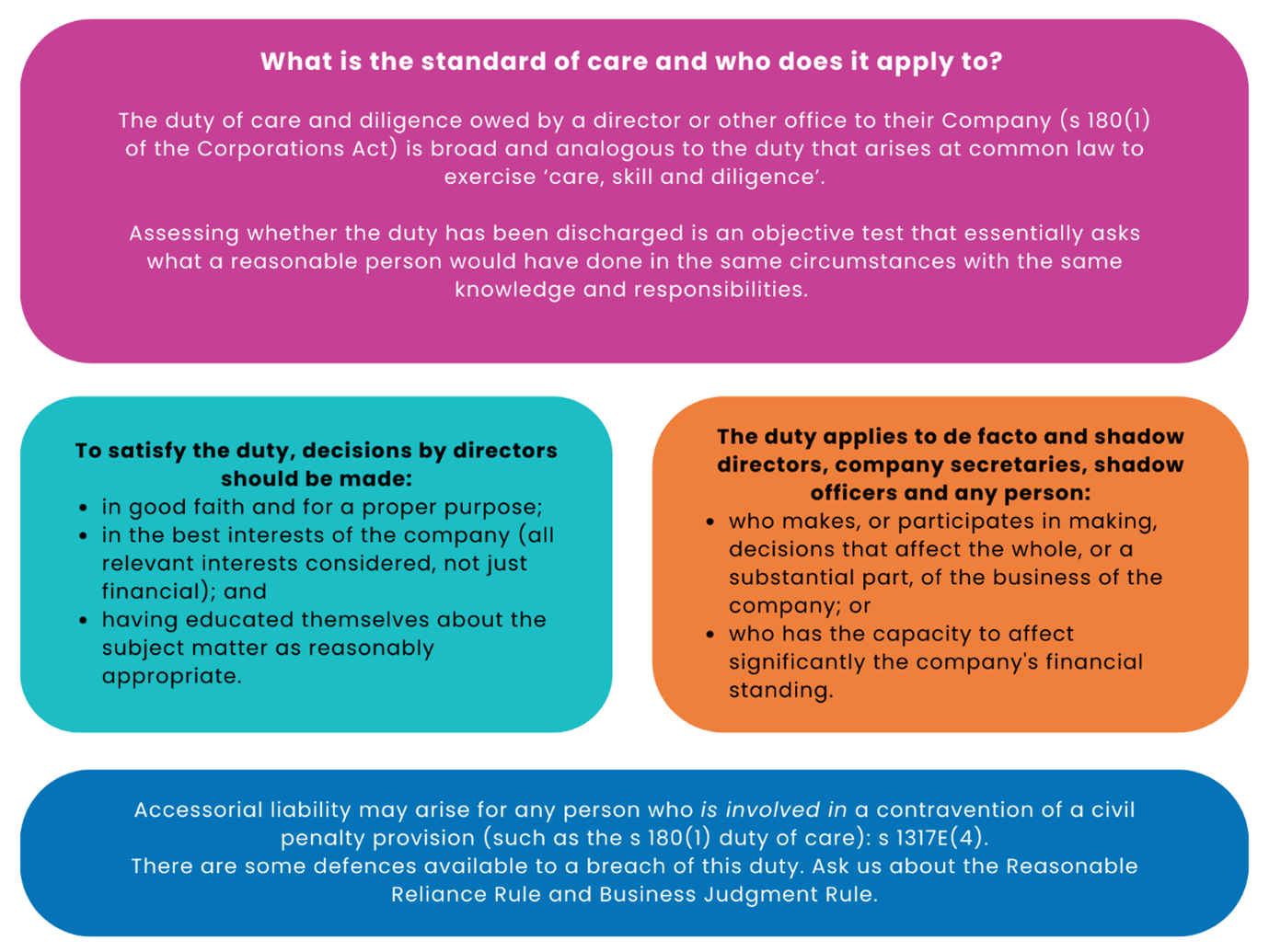

Corporations Act Director Duties

Other statutory director duties also exist (such as in relation to company tax obligations) and these duties also overlap with duties that arise at general law. |

In the line of duty

Corporate liability is often attributable to or associated with director misconduct or neglect. It is therefore unsurprising that where ASIC considers a company has breached its statutory obligations, directors frequently find themselves in the crosshairs for breaching their duties.

Continuous disclosure obligations

ASIC’s recent update on its enforcement action and priorities, highlights an ongoing focus on continuous disclosure obligations as part of its pursuit of broader enforcement priorities.

A prime example is the recent proceedings ASIC brought against Australian Mines Limited and its Managing Director, Benjamin Bell.

Australian Mines Limited (ASX: AUZ) is a listed mining and exploration company which is principally based in Western Australia. Its major asset is a scandium, cobalt and nickel deposit near Greenvale, Queensland about 250km west of Townsville, called the Sconi Project.

The proceedings concerned the conduct of Australian Mines and Mr Bell in relation to presentations given by Mr Bell at overseas investor conferences, where he made unfounded representations regarding Australia Mines’ ability to fund the Sconi Project and overstated the value of its major asset (an offtake agreement).[2]

Earlier this year, Australian Mines was handed a $450,000 penalty by the Federal Court for breaching its continuous disclosure obligations.[3]

Continuous Disclosure Obligation

A listed entity must immediately notify the ASX of any information concerning the entity of which becomes aware (as defined in Listing Rule 19.12) if a reasonable person would expect the information to have a material effect on the price or value of the entity's securities: Corporations Act Chapter 6CA; ASX Listing Rule 3.1.

The penalty was issued after Australian Mines failed in its obligation to disclose material information to the market, by failing to disclose:

- a key term of an offtake agreement to purchase the expected cobalt and nickel product from the Sconi Project;[4]

- the true status of funding for the Sconi Project (after Mr Bell falsely claimed at investor conferences in Hong Kong and London that Australian Mines had secured funding to construct a plant for the Sconi Project, expected to cost $500 million or more, when in fact no funding had been secured); and,

- the true value of the offtake agreement (as the value given failed to take into account a potential buyers discount).[5]

The Court found that the statements were ‘false’ and ‘materially misleading’ to the market, and ‘concerned matters of evident importance for shareholders.'

In addition to the proceedings against Australian Mines for breaching its continuous disclosure obligations, ASIC also sued Mr Bell for breaching the duty of care and diligence he owed to the company.

After judgment was entered against Australia Mines, it seems Mr Bell was left with little option but to admit that he breached his duty of care and diligence by making false statements (regarding funding status and the value of the offtake agreement).

He also breached his duty by failing to cause Australian Mines to correct the false representations or inform the ASX of the true circumstances, even after the ASX had made inquiries.

In short, Mr Bell caused the company to breach its continuous disclosure obligations, and as a consequence has been fined $70,000, disqualified from managing Corporations for 2 years and ordered to pay $60,000 towards ASIC’s legal costs.[6]

'Continuous disclosure obligations are fundamental principles of fairness and transparency that sit at the heart of Australia’s financial markets. When directors fail in their obligations, they undermine these core principles and ASIC will look to take action.’ - Sarah Court, Deputy Chair of ASIC.

Maintenance of financial records – company obligations; director duties

Another example of company obligations that will put the spotlight on directors are internal record-keeping obligations, such as the duty to maintain financial records[7]. The obligation requires companies to keep records that:

- are written;

- correctly record and explain the transactions and financial position and performance of the company;

- would enable true and fair financial statements to be prepared and audited; and

- must be kept for 7 years

Financial Records

In the Corporations Act, financial records include invoices, orders, bills, cheques, promissory notes, and working papers needed to explain financial statements and adjustments made to financial statements.

Corporations are also required to prepare annual financial reports that consist of specific information[8] and include a directors’ declaration. Directors take “particular responsibility” or “overall responsibility” for the company’s financial reports. This derives from:

- the position of director;

- the responsibility placed upon directors by the Corporations Act in the context of financial statements; and

- court judgments which require directors to take a diligent and intelligent interest in the information available to them or which they might appropriately demand from the company’s executives, employees or agents.[9]

If a director breaches their duties by failing to ensure the company maintains financial records, there can be severe consequences.

What are the consequences for a breach of a director duty?

A director is personally liable for a breach of directors' duties. Depending on the duty breached and the nature of the breach, a director may commit a criminal offence (with a maximum penalty of up to 15 years imprisonment), face personal liability for civil penalties, compensation orders for debts and financial losses, and may be disqualified from managing corporations.

Recently[10], ASIC took action against a Victorian director of 3 insolvent companies, after finding that she had failed to:

- act in the best interests of one company, by executing finance agreements that were in the interests of another company that she owned;

- ensure available funds were set aside for an existing tax liability;

- have the companies pay their tax debts;

- ensure a company complied with its obligations to maintain written financial records; and

- prevent a company from incurring debts when there were reasonable grounds to suspect its insolvency.

The director also improperly relied on others to govern her business without adequate oversight.

ASIC disqualified the director from managing corporations for three and a half years.

‘Stepping Stone’ Approach

The ‘stepping stone’ approach to director liability - when a Company is found to be liable for breaching its corporate obligations (step 1), a director is often found personally liable for breaching their duty to the company by having allowed or having caused the Company to breach its legal obligations (step 2).

Take away - directors - know your duties

These cases highlight ASIC’s recent focus on ensuring adequate financial records are kept, and continuous disclosure obligations are complied with, and highlight the importance of directors and officers complying with their duties. To do this, directors must know what their duties are and what they require in the circumstances of their company and corporate structure.

To ensure accurate financial records are kept, directors and officeholders should be conscious that they cannot blindly rely on management.

To ensure compliance with continuous disclosure obligations, directors and officers must give careful and continuous thought to what matters they may need to update the ASX and market about, and what information should and should not be disclosed to investors.

Regulatory Guide 198 Unlisted disclosing entities: Continuous disclosure obligations by ASIC, is a helpful guide available on ASIC’s website.

In circumstances of uncertainty or a potential dispute, please get in touch.

[1] ASIC InFocus September 2023 - Volume 32 Issue 7.

[2] ASIC’s Concise Statement dated 10 May 2022 [3].

[3] Australian Securities and Investments Commission v Australian Mines Limited [2023] FCA 9.

[4] A buyer’s discount of 15% upon the buyer acquiring Australian Mines shares at a fixed price.

[5] ASIC MEDIA RELEASE (23-004MR). Mr Bell misleadingly stated at the same two investor conferences that the value of the offtake agreement was $5 billion, despite the agreement including a potential buyers discount of 15%.

[6] ASIC MEDIA RELEASE (23-125MR)

[7] Corporations Act 2001 (Cth) s 286.

[8] See, for example, sections 295, 296 and 297 of the Act.

[9] See, for example: Australian Securities and Investments Commission v Healey (2011) 196 FCR 291; 83 ACSR 484; 29 ACLC 11-067; [2011] FCA 717.

[10] ASIC MEDIA RELEASE (20-240MR).